6x Earnings, 7% Dividend, 76% ROCE, No LT Debt

Globrands (GLRS.TA) is Israel’s second-largest tobacco distributor. They have exclusive distribution agreements with Japan Tobacco International — a relationship going back 25 years — and British American Tobacco (19 years) to import cigarettes and distribute them to 10,000+ retail points across Israel via a direct Van Sale fleet. Three of the top ten best-selling cigarette brands in Israel are theirs.

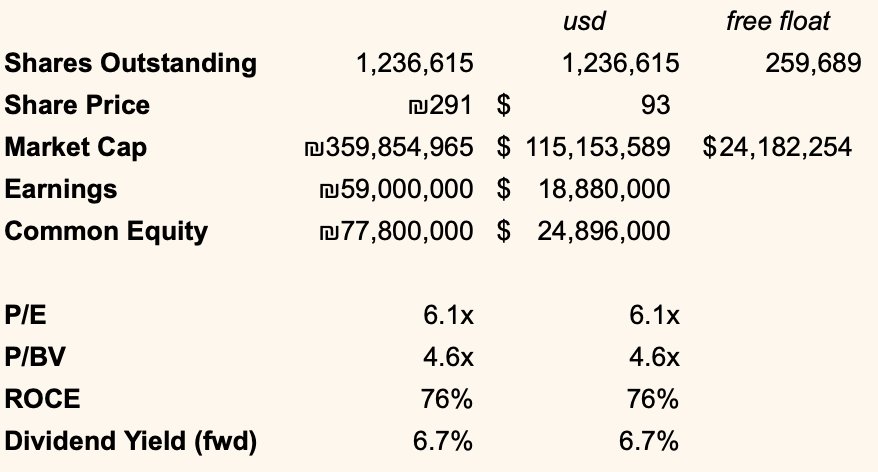

Yaron Gazit — Chairman of the Board — owns 40.5% of the company. After accounting for other insider ownership, only ~21% of the float is free. That’s around $24M. Not something many hedge funds are going to look at.

The business earned ₪59M attributable to common shareholders on ₪77.8M of equity in FY2025. Pay 4.6x book for a business earning 76% ROE, and you're getting a 16.5% earnings yield.

Here’s the problem.

The contract with JTI — which represents roughly 45% of Globrands’ net revenue — expires in February 2027. Globrands disclosed that JTI is simultaneously negotiating with several other parties interested in distributing JTI products in Israel.

The contractual history with JTI is worth understanding in detail, because it explains both the current situation and the range of outcomes.

In December 2018, after Globrands’ IPO exposed its profitability, JTI demanded a renegotiation that would reduce Globrands’ profit on JTI products by 33% cumulatively by 2024 — imposed at 4% annually in 2019–2020 and 9% annually from 2021 through the contract’s end.

In that same month, Globrands disclosed it had reached agreement with JTI to extend the relationship by six years from February 2021 to February 2027. In February 2020, the companies formally signed the extension. In that same filing, JTI explicitly told Globrands that removing an older clause did not indicate any plan by JTI to self-distribute in Israel or appoint another distributor.

On February 2, 2026, Globrands disclosed that it is in negotiations with JTI over contract renewal. The filing states that to the best of Globrands’ knowledge, JTI is conducting similar negotiations with several other parties interested in distributing JTI products in Israel.

It warns that even if a new agreement is signed, Globrands’ annual profit rate on JTI products is expected to decline versus 2024 and 2025 levels. There is no certainty the agreement will be renewed at all.

The filing also confirms that the JTI margin cap — the ceiling on Globrands’ share of net revenues from JTI products — remains unchanged for 2025 and 2026, meaning the financial deterioration from any renegotiation begins only from February 2027.

Globrands has provided JTI with a ₪45M bank guarantee, up from the original ₪30M threshold, reflecting growth in order volumes.

That’s the reason the stock is at 6x earnings, down 50% from its high.

This is a binary outcome. If JTI renews, even at renegotiated terms — the stock is cheap. If JTI walks, there’s a ₪357M revolving credit facility used for working capital that would need to be renegotiated, but they have basically no long-term debt (₪4M).

We should know in the next 6–12 months.

Odds are JTI signs a new contract with Globrands but on worse terms. At 6x earnings, worse terms are priced in.

DISCLAIMER: Global Value AI LLC is not a registered investment advisor, broker-dealer, or financial planner. Nothing published here constitutes investment advice, a solicitation, or a recommendation to buy or sell any security. All content is for informational and educational purposes only. We may hold positions in securities discussed. Do your own research. You are solely responsible for your own investment decisions and any gains or losses that result from them.